- Global financial conditions have improved across the world, although rising debt levels pose a future threat.

- An uneasy cessation of trade hostilities between China and the United States provided some relief.

- The bright spot in the global economy continues to be consumer spending.

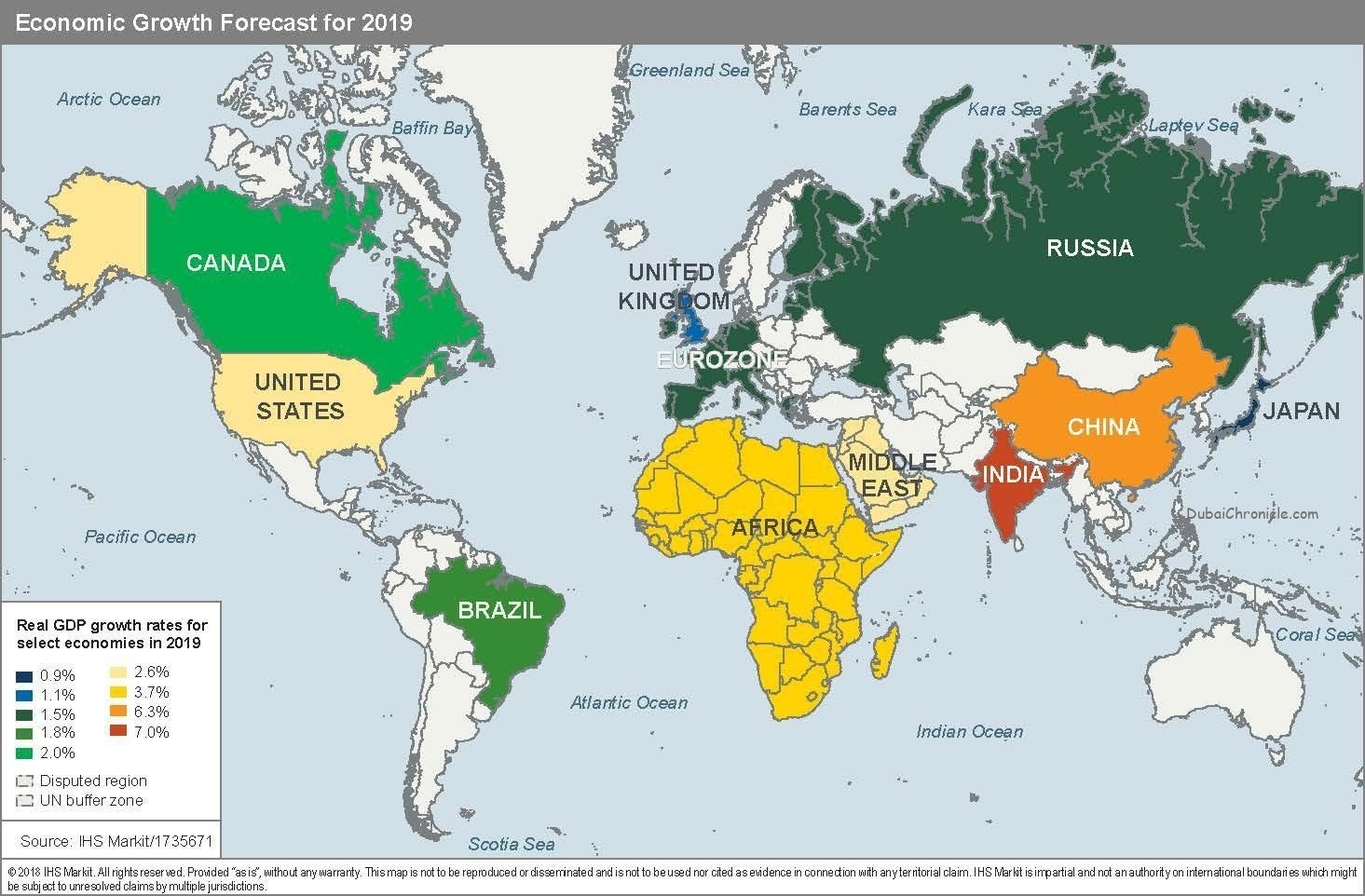

Global growth weakened considerably in 2019 as trade wars and weakening growth in China negatively impacted growth. In many parts of the world, the manufacturing sectors were either in recession or close to recession territory. In response, many central banks began to loosen monetary policy – rather than tighten as had been expected a year ago – with some countries (notably China and the United States) providing additional stimulus as well.

However, the past month has seen some relief in the unrelentingly downbeat news on the global economy: an uneasy cessation of trade hostilities between China and the United States, the diminished risk of a no-deal Brexit, and an ease in financial conditions, as stimulus provided by central banks is beginning to filter through.

Meanwhile, as global exporters adjusted to the new world of higher tariffs, the impacts of the trade war on real GDP growth turned out to be smaller than expected. By the end of the year, many of the IHS Markit purchasing managers’ indexes (especially in manufacturing) began to stabilize and show small gains.

Moreover, while any major progress on the trade war will likely have to wait until after the 2020 US elections, an escalation in hostilities – significant enough to do major damage – also seems unlikely. The bright spot in the global economy continues to be consumer spending, which is benefitting from decent income growth, along with low oil prices, inflation, and interest rates. In addition, global financial conditions have improved across the world, although rising debt levels pose a future threat. All told, IHS Markit expects global growth to stabilize at 2.5% in 2020, before edging up in 2021 and 2022.

The US economy will grow at trend – around 2%

IHS Markit analysts assess the trend, or potential, growth in the US economy to be around 2%. Real GDP growth was above trend from 2017 to 2019 thanks to fiscal stimulus. However, with the effects of this stimulus wearing off, growth is returning to trend. Some special factors will boost GDP growth over the first half of next year; the “phase one” trade deal with China will also help a little. Consumer spending – roughly 70% of the economy – will increase about 2.7% in 2020, putting a floor on growth in the broader economy. On a calendar-year basis, we look for real GDP to expand 2.1% next year.

China’s growth rate will fall below 6%

While it is tempting to blame much of the recent slowdown on the US-China trade war, the decade-long deceleration is the result of both structural and cyclical factors: an ageing population and a sharp drop-off in productivity growth mean that potential growth in China is lower now than a decade ago and is set to fall further.

Since the global financial crisis 10 years ago, China’s debt as a percentage of GDP has surged to about 260% – mostly due to a corporate borrowing binge and more recently an increase in household mortgage borrowing – tying the hands of policymakers.

Attempts to deleverage the economy by curbing the role of shadow banks have only been partially successful and have come at the expense of growth. Policymakers are currently engaged in a balancing act: they would like to cut the debt ratio (or at least keep it from rising), while providing enough stimulus to keep growth from falling too fast. IHS Markit predicts that China’s growth rate will slide even further, to 5.7%, in 2020.

Europe’s economy will stabilize, then recover slightly

The slump in eurozone growth in 2019 was alarming, nevertheless, there are some signs that the worst may be over. While the “hard” data are giving mixed signals (weakness in the business sectors versus sustained growth in consumer spending), the “soft” data are showing early signs of an inflection point. In particular, the IHS Markit manufacturing PMIs for the eurozone have picked up a little – although service-sector PMIs have weakened. IHS Markit expects eurozone growth to stabilize at around 0.9% in 2020, before picking up a little in 2021.

Meanwhile the results of the UK election suggest that while the worst of the Brexit uncertainty may be over, there is still a hard slog ahead, with growth dropping to 0.5% in 2020, before recovering slightly in 2021.

Japan’s faltering growth will be cushioned by more stimulus

Japan’s real GDP growth rate accelerated to an estimated 1.1% in 2019. However, fourth-quarter growth is expected to turn negative as a result of the increased sales tax at the beginning of October. In response to the weakness driven by the sales tax hike, along with the drag from trade and super Typhoon Hagibis, the Abe government announced a larger-than-expected $120 billion, 15-month fiscal package – the first since 2016 and the largest since 2012.

The money, intended to upgrade infrastructure, invest in new technologies, and repair typhoon damage, will neutralize much of the negative effects of the sales tax hike. Consequently, after falling to 0.3% in 2020, Japanese real GDP growth is projected to recover in 2021.

Emerging markets will continue to tread water, as debt reaches new peaks

The past decade has not been kind to the emerging world, as growth has fallen from an average 7.3% in 2010 to 4.2% in 2019. While the long slide in China’s growth rate has been a key factor, emerging markets also faced two other stiff headwinds: lackluster expansions in the developed world and falling commodity prices.

Recoveries in the developed world are predicted to remain fragile in the next few years, while commodity prices are expected to slide, at least in the near term. These, along with the simmering trade war and the continued decline in China’s rate of expansion, mean that there is very little scope for growth in the emerging world to rise much – if at all – from current low rates. More local concerns, such as riots in Latin America and faltering growth in India are also worrisome.

{kind=link}